Florentia | Issue 66

Trade Chokepoints, Aldi’s Ascent, China’s Ports, and AI Chocolate

Happy Monday and welcome back to Florentia.

Florentia is a blog that showcases innovations and opportunities across our food, health, and environmental systems. In particular, Florentia focuses on topics at the intersection of food and other industries (healthcare, energy, manufacturing, etc).

Florentia is structured in two parts: (1) bi-weekly Monday newsletters with news, perspectives, funding announcements, interviews, and more from around the industry and (2) periodic Sunday deep dives into pressing topics.

You’re reading Monday newsletter #66. Let’s dive in.

Content I’ve Enjoyed the Last Two Weeks 🧬 🌳 🧱

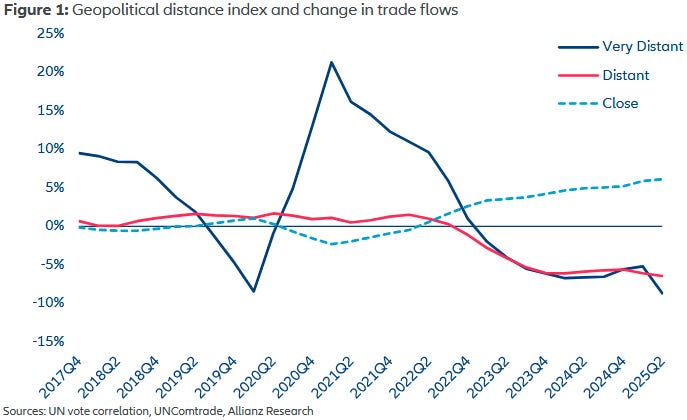

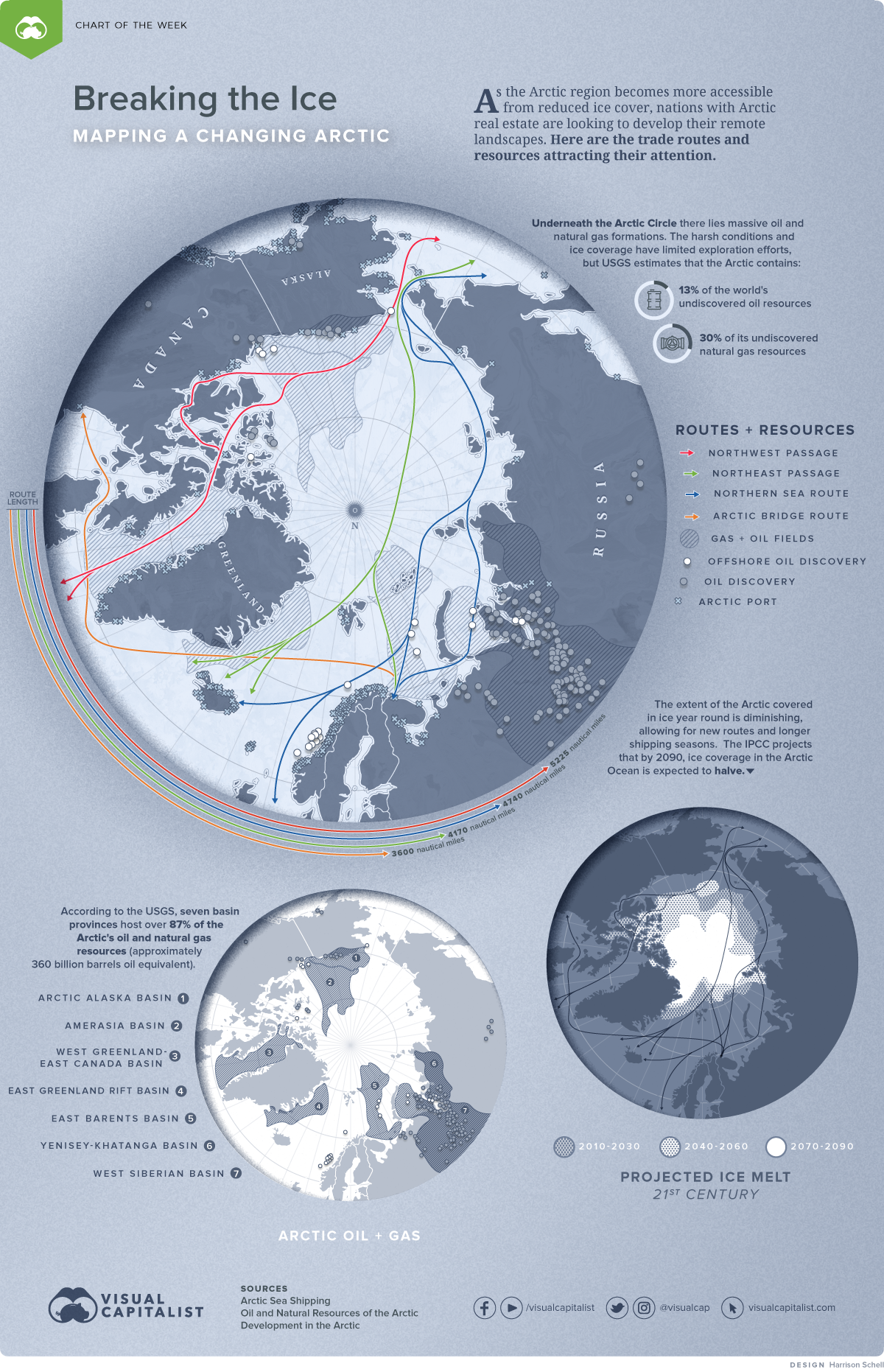

Old trade routes for new trade wars? [Allianz Trade]

Geopolitics and security is rewiring international trade, an industry driven historically by pure cost minimization. Over the past 10 years, trade fell significantly between less politically aligned countries, with the US shifting from China, the EU from Russia, and China pivoting to the Global South.

Alliances are shaping staple flows (grains, oilseeds, fertilizer, feed, meat), instead of just yields and prices.

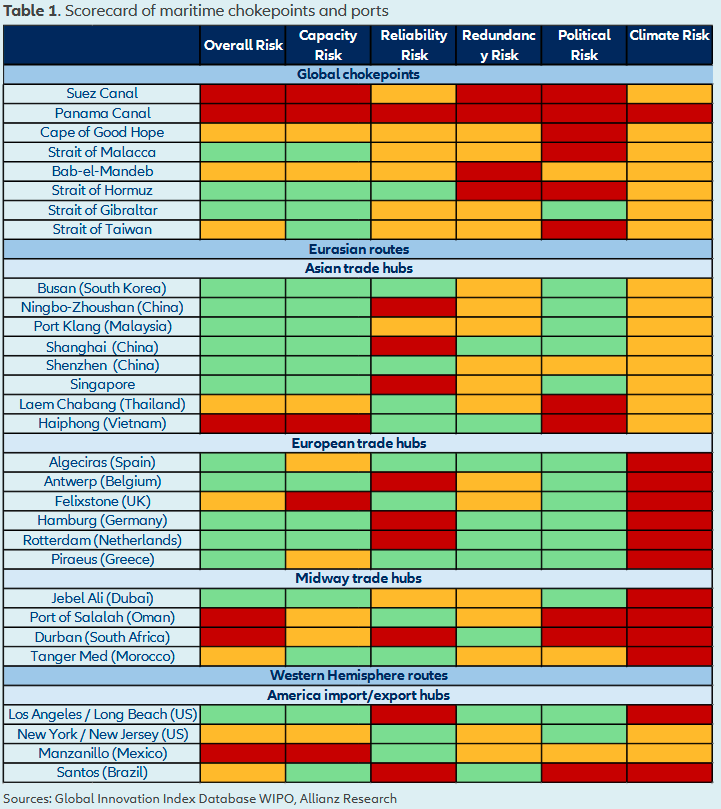

This phenomenon is starkly apparent in declining trends in the “old, core routes”. The Suez, Panama, Malacca, and Hormuz carry about 50% of global trade, but are increasingly being hit with conflict risk and climate shocks. Investors are seeing these logistical choke points as riskier, and thereby pricier.

As a result, new “bypass” corridors are scaling up:

Asia: The Trans‑Caspian Middle Corridor linking China–Central Asia–the Caucasus–Europe has cargo up 80%+ YOY.

Africa: Detours around the Cape of Good Hope have become a semi‑permanent alternative to the Red Sea, up 191% from last year.

South America: Chancay in Peru is funded explicitly to move critical minerals and agribusiness exports to China and ASEAN.

Nearshoring: The US–Mexico and India–Middle East–Europe corridors continue to be built out.

This is also a big reason why geopolitical tension over Arctic trade routes has been heating up (no pun intended).

Aldi effect sweeps US supermarkets as shoppers embrace private label [Financial Times]

The US grocery industry is undergoing a structural shift that makes it look more like western Europe: private label is steadily taking share from national brands.

Aldi and Lidl’s discount model (limited assortment, high private label penetration, ruthless cost discipline) is scaling in the US and taking mainstream players with it. Private label food sales are growing much faster than national brands, with US private-label penetration still trailing western Europe by >20%.

In theory, there’s over a $100bn left in “catch-up” sales.

Private label brands have not only become “satisfactory” for consumers, but are actually sought out by some (ie Kirkland). Some somewhat shocking numbers (for me at least) to put to this:

Aldi

The average US family of four who bought branded products spent $10,610 per year, but only $6,759 when buying Aldi’s private label.

75% of shoppers said Aldi’s brands were “just as good as more expensive brands”.

Costco

Their private label, Kirkland, recently hit $86B in sales.

33% of Costco’s sales are private label.

Walmart

1/4 of their annual net sales come from private label brands, including Great Value.

A clear power shift in the value chain here. And definitely some opportunity in the co-manufacturing space.

Some Interesting Reads (hover for link) 🥗 📦 🦾

The number of infant botulism tied to baby formula has climbed to 15. Here’s what to know: New baby formula-tied botulism outbreak reopens questions about infant formula safety, ingredients, and viability of small challengers the market. [AP]

Trump’s Global Trade Chaos Creates Opportunity for African Farmers: Trade war fallout and food-security fears drive billions into African agriculture, promising yield gains, but big execution and “land grab” risks. [Bloomberg]

Doctors find Fresh Evidence that Fruits and Vegetables Can Act as Powerful Medicines: “Food Is Medicine” trials find produce prescription programs cut blood pressure ~5 points. [NPR]

Meet the Man Building a Starter Kit for Civilization: A “civilization starter kit” of open-source, repairable machines reframes farm equipment as modular infrastructure. [MIT Technology Review]

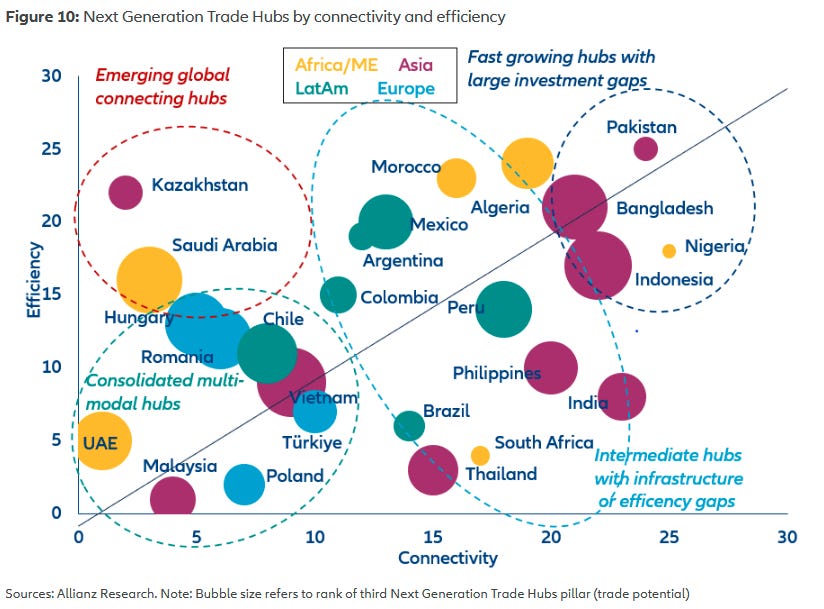

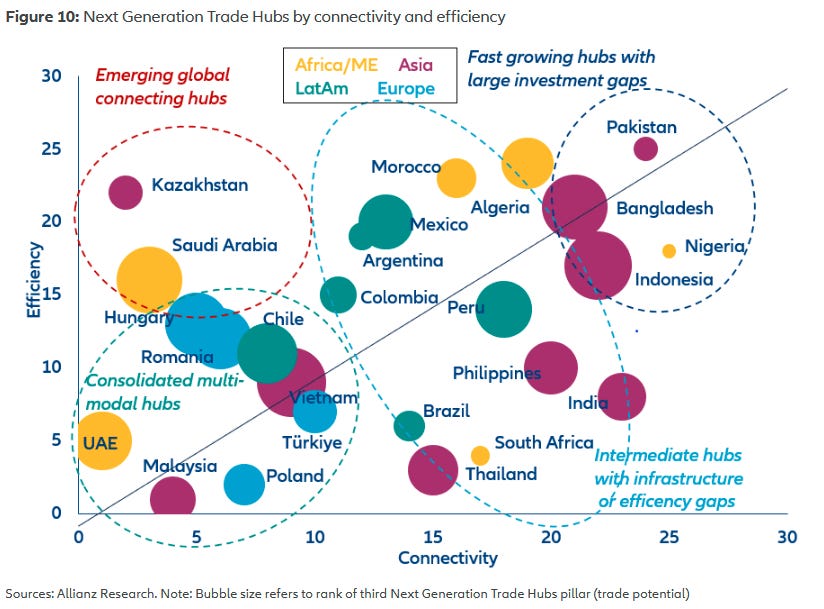

China’s Network of Shipping Ports is Too Big for Trump to Unravel: Chinese firms now control terminals at 90+ overseas ports, turning logistics infrastructure into a geopolitical pressure point for US- and LATAM–linked food supply chains. [Bloomberg]

Disrupting the first reported AI-orchestrated cyber espionage campaign: A Chinese state-backed group launched a near-fully automated cyber attack using Claude AI Agents. [Anthropic]

Trump removes tariffs on Brazil coffee, beef: US grants retroactive exemptions on Brazilian ag imports, especially coffee, easing price pressure as trade and political tensions persist. [Food Dive]

Barry Callebaut to use NotCo’s AI for Chocolate Recipes: Barry Callebaut teams with NotCo to use AI for chocolate formulations and cocoa-free alternatives as cocoa prices jump ~30% since early 2024. [Food Dive]

Trump Administration Considers Bringing Back the Food Pyramid: New guidelines may replace MyPlate, elevating meat and dairy while challenging decades of low-fat orthodoxy. [Bloomberg]

Scoop: Unilever looks to divest food business in Europe: Working with Houlihan Lokey to divest parts of its EU food business, Unilever continues the shift away from legacy grocery brands toward higher-growth categories. [Axios]

Finance & Transactions 🏦 💵

Function Health raises $298mm Series B at $2.5B valuation (11.19.2025)

Biocentis Raises $19mm (11.19.2025)

Erg Bio Raises $6.5mm (11.18.2025)

Keychain Raises $10mm (11.17.2025)

Gopuff Raises $250mm (11.13.2025)

That’s all for this week! Thanks for reading. Be a friend, tell a friend.

See you in two weeks! 👋